Last Updated: February 2026

Most crypto investors diversify the wrong way. They buy ten different tokens, feel protected, and watch their entire portfolio drop 70% in the same bear market. This is called diworsification — the illusion of diversification without its actual benefits. The ten tokens were all highly correlated; when Bitcoin fell, everything fell with it.

Real diversification is a mathematical discipline. Harry Markowitz proved this in 1952 in his groundbreaking paper Portfolio Selection — work that earned him the Nobel Prize in Economics in 1990. His insight: the expected return of a portfolio is simply the weighted average of its components’ returns, but its risk is less than the weighted average of individual risks — if the assets are not perfectly correlated. The lower the correlation, the more risk you eliminate by combining assets.

In 2026, crypto offers enough asset diversity — large-caps, DeFi, Real-World Assets, stablecoins, multi-chain ecosystems — to build genuinely Markowitz-optimized portfolios. This guide shows you how.

Why Diversification Works: The Math

Crypto volatility is not a rumor. Bitcoin’s annualized volatility has historically ranged between 60% and 80%, compared to the S&P 500’s long-run average of around 15%. Individual altcoins routinely see 90%+ drawdowns in bear markets. This is the environment you are operating in.

The naive response is to hold fewer assets and pick the best ones. The mathematically correct response is to hold assets that move independently of each other. When Asset A falls 40%, Asset B might only fall 10% — or even rise — because it responds to different market forces. Your combined portfolio falls far less than either asset alone.

This is not intuition. It is Nobel Prize-winning mathematics. The portfolio variance formula — σ²p = Σᵢ Σⱼ wᵢ wⱼ σᵢ σⱼ ρᵢⱼ — shows that portfolio risk depends critically on the correlation coefficient ρᵢⱼ between each pair of assets. When correlations are low (ρ close to 0) or negative (ρ below 0), combining those assets dramatically reduces total portfolio risk without sacrificing the weighted average return.

The measure that matters most for a diversified portfolio is the Sharpe Ratio: (portfolio return − risk-free rate) / portfolio volatility. It tells you how much return you earn per unit of risk taken. Research from asset managers including WisdomTree has shown that even a small Bitcoin allocation to a traditional 60/40 portfolio significantly improves its Sharpe ratio — not because Bitcoin alone has a great Sharpe ratio, but because its low correlation to bonds and moderate correlation to equities improves the portfolio combination.

Know Your Risk Profile Before You Allocate

Audit Your Wallet — Get Your On-Chain Risk Profile Free

Before building a diversified portfolio, understand where you actually stand. ChainAware Wallet Auditor gives you your Experience Level, Risk Willingness, Predicted Intentions, and Credit Score — all from your on-chain history. No KYC. Free. Instant.

Modern Portfolio Theory and the Efficient Frontier

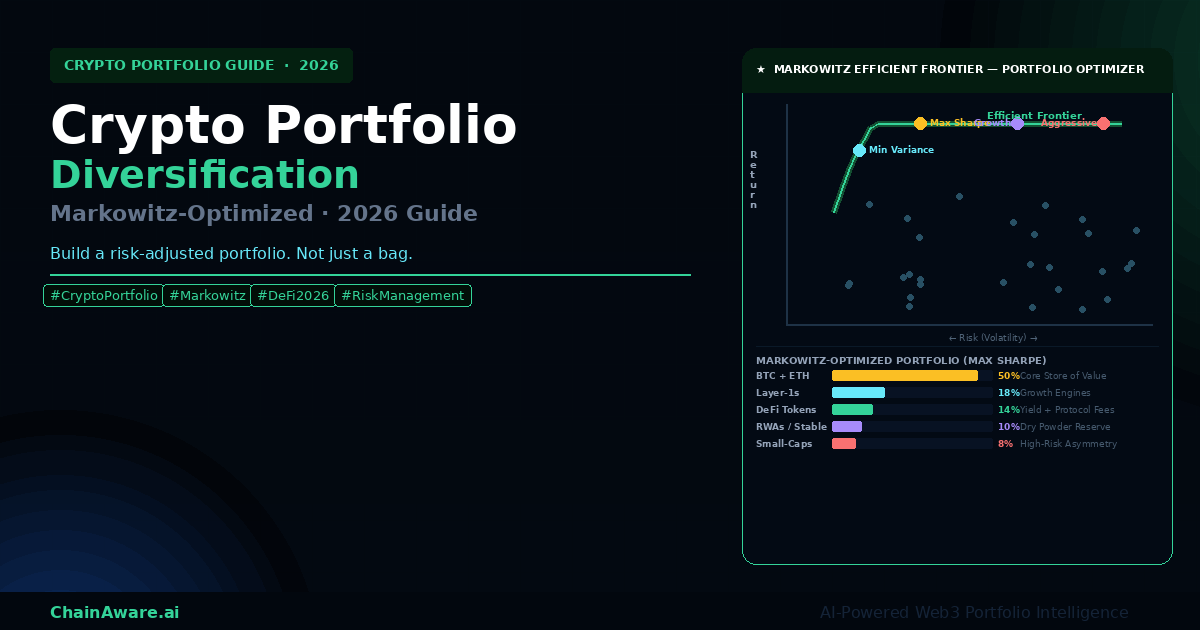

Markowitz’s Modern Portfolio Theory (MPT) gives us a precise framework for portfolio construction. The central concept is the Efficient Frontier: the set of portfolios that offer the maximum possible expected return for every given level of risk. Any portfolio that lies below the Efficient Frontier is suboptimal — you could get either more return for the same risk, or the same return for less risk, by reallocating.

The Three Key Inputs

To construct an efficient frontier, you need three inputs for each asset in your portfolio.

Expected return — the anticipated annualized return, estimated from historical returns or fundamental analysis. For Bitcoin, long-run analysts in 2026 often reference 4-year cycle return patterns. For DeFi tokens, expected returns incorporate both price appreciation and protocol yield.

Expected volatility (standard deviation) — how much the asset’s price fluctuates. Bitcoin’s historical annualized volatility sits around 60-80%. Ethereum is similar. DeFi tokens can be 100-200%. Stablecoins are near zero. RWA tokens are typically 10-30%, closer to their underlying traditional asset.

Correlation matrix — the pairwise correlation coefficients between every combination of assets. This is where crypto portfolios offer real opportunity. The BTC/ETH correlation is high (~0.85), meaning they move together and don’t provide much diversification benefit relative to each other. But BTC vs. stablecoins has near-zero correlation. BTC vs. tokenized treasury RWAs has a correlation of roughly 0.15-0.30. These low-correlation assets are where real diversification benefit comes from.

The Efficient Frontier in Practice

Once you have these inputs, portfolio optimization software (or a Python library like pypfopt) computes the full set of efficient portfolios by solving a quadratic optimization problem: minimize portfolio variance subject to a target return, across all possible weight combinations. The result is a curve in risk/return space — the Efficient Frontier.

Two portfolios on the Efficient Frontier are particularly important. The Minimum Variance Portfolio sits at the leftmost point of the frontier — the portfolio with the lowest achievable risk. In crypto in 2026, this tends to be heavily weighted toward stablecoins and Bitcoin with small allocations to RWAs. The Maximum Sharpe Ratio Portfolio (also called the Tangency Portfolio) sits where a line from the risk-free rate is tangent to the frontier — this is the portfolio with the best risk-adjusted return. For most crypto investors, this is the optimal target.

Research from academic studies on crypto portfolio optimization consistently finds that mean-variance optimized crypto portfolios outperform naive equal-weight or market-cap-weight portfolios on a risk-adjusted basis over multi-year periods — particularly when stablecoins and low-correlation assets are included.

The Markowitz-Optimized Crypto Portfolio (2026 Target Allocation)

Based on historical return, volatility, and correlation data through early 2026, a Maximum Sharpe Ratio portfolio for a crypto-native investor targeting long-term growth typically resembles the following structure. This is a starting point — your personal risk tolerance, time horizon, and existing holdings will adjust these weights.

Bitcoin + Ethereum (50%) — the core. These are the market’s largest, most liquid assets with the most established long-run return records. They are highly correlated with each other (~0.85) but serve as the portfolio’s stable foundation. BTC functions as digital gold and macro hedge; ETH captures DeFi ecosystem growth and yield from staking.

Layer-1 Protocols (18%) — growth engines with partially differentiated correlation to BTC/ETH. Solana, Avalanche, and emerging Layer-1s respond to ecosystem-specific adoption signals. Their correlation to BTC is moderate (~0.65-0.75), providing partial diversification while maintaining crypto market exposure.

DeFi Tokens (14%) — protocol tokens from leading DeFi platforms (lending, DEXes, yield aggregators). DeFi tokens carry higher volatility than large-caps but generate yield through protocol fee distributions. Their correlation to BTC is moderate (~0.60-0.70) with significant idiosyncratic risk — a protocol that grows TVL outperforms regardless of macro crypto sentiment.

Real-World Assets and Stablecoins (10%) — the diversification anchor. Tokenized treasuries, tokenized real estate, and stablecoins carry near-zero correlation to crypto markets. In MPT terms, adding even a 10% allocation to a near-zero-correlation asset substantially reduces total portfolio variance. According to RWA.xyz data, tokenized RWA markets reached $15+ billion in 2025 and are growing rapidly, providing genuine on-chain access to low-correlation yield-bearing assets.

Small-Cap Altcoins (8%) — asymmetric upside. A small allocation to high-conviction small-cap positions captures the fat tail of crypto return distributions — the 10x-100x outcomes — while limiting downside impact to 8% of total portfolio. This is not random allocation; it requires fundamental analysis of the project’s product, team, and token economics.

AI-Powered Portfolio Intelligence for Developers and DeFi Power Users

Prediction MCP: Query Any Wallet’s Risk Profile in Real Time

Build AI agents that query ChainAware’s behavioral database for any wallet — experience level, risk willingness, fraud probability, credit score, and predicted next action. Integrate portfolio-aware intelligence directly into your DeFi app, lending protocol, or analytics dashboard.

Crypto Asset Correlation in 2026

Correlation is the most important and most overlooked variable in crypto portfolio construction. Understanding which assets move together — and which don’t — is what separates real diversification from the illusion of it.

In 2026, the crypto correlation landscape has several consistent patterns. BTC and ETH remain highly correlated (~0.82-0.88) — they move together during macro risk-on and risk-off events. Most major altcoins are moderately correlated with BTC (0.60-0.80) during normal market conditions, but correlations spike toward 1.0 during sharp selloffs (the “correlation convergence” effect well-documented in risk literature). Stablecoins have near-zero correlation to all crypto assets. Tokenized RWAs maintain low to moderate correlation (0.15-0.35) with crypto depending on the underlying asset type — tokenized treasuries are closer to zero; tokenized real estate somewhat higher.

The practical implication: a portfolio of BTC, ETH, and ten altcoins is far less diversified than it appears. Adding a meaningful stablecoin reserve and RWA allocation provides genuine correlation benefit. The goal is not maximum number of assets but maximum spread of the correlation matrix.

Practical Diversification Methods

Market-Cap Tiering

The most accessible entry point to diversification is allocating across different market-cap tiers. Large-caps (BTC, ETH) provide stability and liquidity — they form the foundation. Mid-caps (top 20-50 by market cap) offer established projects with proven product-market fit and stronger growth potential. Small-caps (outside top 50) offer high risk/high reward with significant downside risk; position sizing here should reflect that only a minority will succeed, but those that do can return 10-100x.

Sector Diversification

The crypto ecosystem has matured into distinct sectors that respond to different catalysts. Layer-1 protocols react to developer activity and ecosystem adoption. DeFi tokens respond to TVL growth, fee revenue, and protocol upgrades. Gaming and metaverse tokens are driven by user acquisition and active gameplay metrics. Infrastructure tokens (oracles, storage, bridges) grow with overall Web3 activity. Real-World Assets grow with institutional adoption and regulatory clarity. Stablecoins offer yield with near-zero volatility. A sector-diversified portfolio captures multiple growth cycles rather than betting on a single narrative.

Multi-Chain Allocation

In 2026, limiting yourself to a single blockchain is an unnecessary concentration risk. Ethereum remains the deepest DeFi ecosystem. Solana has established itself as the consumer-facing chain for high-frequency trading and retail apps. Base, Arbitrum, and Optimism offer Ethereum security with lower costs. BNB Chain provides access to a large retail user base. Haqq Network serves the Islamic finance market. Accessing yield and protocol opportunities across multiple chains reduces smart contract risk (a single chain exploit doesn’t wipe your whole portfolio) and captures chain-specific growth.

For an overview of how to assess wallet activity and behavior across all 8 supported chains, see the ChainAware Wallet Auditor complete guide.

Stablecoin Reserve Strategy

Holding 10-20% in high-quality fiat-backed stablecoins (USDC, USDT) serves two functions that are often undervalued. First, it reduces portfolio volatility directly — stablecoins are the only zero-volatility asset in crypto. Second, it provides “dry powder” for opportunistic buying during market dislocations. Some of the best returns in crypto come not from picking assets but from having capital available to deploy at the market bottom. In MPT terms, stablecoins shift the Efficient Frontier leftward — your maximum achievable Sharpe ratio increases with a stablecoin allocation up to a point.

Your On-Chain Financial Profile — Instant, Free

ChainAware Credit Score: Unlock DeFi Lending Based on Your Portfolio Behavior

A well-diversified, consistently managed portfolio builds a strong on-chain credit profile. ChainAware Credit Score analyzes your Wallet Auditor profile + Fraud Risk + Cash Flow to generate a 0–1000 score. High scores unlock undercollateralized lending — borrow at 75-90% LTV without locking up excess capital.

Using Wallet Intelligence to Diversify Better

One under-utilized input for portfolio decisions is your own on-chain behavioral profile. Your transaction history reveals patterns about your risk tolerance, experience level, and how you actually behave under market stress — which may differ from how you think you behave.

The ChainAware Wallet Auditor surfaces this profile. It gives you five dimensions: your Experience Level (how sophisticated your on-chain activity is), your Risk Willingness (how much actual risk your historical trades reflect), your Predicted Intentions (what you’re likely to do next based on behavioral patterns), your Wallet Rank (composite quality vs. 14 million+ profiled wallets), and your AML Status. This profile is the honest answer to “what kind of investor am I?” — which is the first question portfolio allocation should answer.

Beyond self-assessment, wallet intelligence matters for counterparty risk. In DeFi lending and P2P transactions, the creditworthiness of the counterparty determines your actual risk. Before lending to a wallet or entering a large P2P trade, checking the counterparty’s credit score via the ChainAware Credit Score guide is the Web3 equivalent of a credit check — and it’s free.

For DeFi platforms wanting to screen the risk profile of their own user base before extending credit or adjusting collateral requirements, the Fraud Detector provides a 98%-accurate behavioral fraud probability for any wallet. Combined with the Wallet Auditor and Credit Score, this gives a complete picture of portfolio counterparty risk that no other tool in Web3 currently provides.

For a deeper look at how on-chain analytics powers smarter Web3 strategies, see our Web3 Behavioral Analytics guide and the ChainAware complete product guide.

Common Diversification Mistakes

Correlation blindness. Holding ten altcoins when all ten have BTC correlation above 0.80 provides almost no diversification benefit. In a sharp market selloff, correlations converge toward 1.0 across all crypto assets except stablecoins and RWAs. True diversification requires assets with genuinely different correlation profiles — not just different ticker symbols.

Narrative chasing. Rotating your entire portfolio into the latest narrative (AI tokens, meme coins, DePIN) concentrates exposure into assets that are typically highly correlated with each other and with BTC, with additional idiosyncratic risk. Reserve narrative exposure for the small-cap asymmetric allocation (8% in the MPT framework above) — not the core portfolio.

Over-diversification (diworsification). Holding 40+ positions makes portfolio management impractical, increases transaction costs, and often reduces returns because the small positions can’t move the needle even when they perform well. Markowitz optimization typically concentrates into 5-10 positions for maximum Sharpe — more is not better.

Ignoring rebalancing drift. A portfolio that starts optimally allocated will drift significantly after a bull run — your small-cap allocation might grow from 8% to 25% of the portfolio after a 5x move. Without rebalancing, you’re no longer holding your optimal portfolio; you’re holding whatever the market left you with.

Neglecting smart contract risk. Even a perfectly diversified token portfolio can be wiped out if all positions are in protocols on a single chain that suffers an exploit. True crypto diversification includes operational security: hardware wallets for long-term holdings, multi-chain distribution to reduce chain-specific risk, and protocol due diligence. For a complete security framework, see our guide to the best crypto hardware wallets in 2026.

Rebalancing: When and How

Rebalancing is the discipline of returning your portfolio to its target allocation after market movements have caused it to drift. In MPT terms, it’s the mechanism that keeps you on the Efficient Frontier rather than drifting into a suboptimal position.

There are two main rebalancing approaches. Calendar rebalancing resets allocations on a fixed schedule — quarterly works well for most crypto investors, balancing responsiveness with transaction cost efficiency. Threshold rebalancing triggers a rebalance whenever any asset drifts more than a specified percentage (e.g., 5 percentage points) from its target weight. Threshold rebalancing is more responsive but generates more transactions and therefore more tax events and gas costs.

A practical middle ground: threshold-trigger quarterly rebalancing. Review the portfolio quarterly, and rebalance at that review only if any allocation has drifted more than 5 percentage points from target. This keeps costs and tax events minimal while maintaining meaningful portfolio discipline.

According to Vanguard research on portfolio rebalancing, the primary benefit of rebalancing is risk control rather than return enhancement — consistent with the MPT framework. The goal is not to time the market through rebalancing but to maintain your intended risk profile as markets move.

AI Tools for Portfolio Optimization in 2026

The computational demands of true Markowitz optimization — estimating return, volatility, and correlation for dozens of assets, then solving the quadratic optimization — are now handled by AI tools that make this accessible to any investor.

ChainAware’s Prediction MCP goes further than portfolio math. It connects AI agents to real-time wallet behavioral profiles across 14 million+ profiled wallets, enabling portfolio construction informed by actual on-chain behavioral intelligence rather than just price data. An AI agent using the Prediction MCP can assess whether a DeFi protocol’s user base is high-quality (experienced, low fraud risk, high credit score) or driven by bots and farmers — a signal that directly affects a protocol’s long-term token value.

For DeFi platforms specifically, see 5 ways Prediction MCP turbocharges DeFi platforms for specific use cases.

For hands-on portfolio trackers and tax software, CoinGecko Portfolio and Koinly remain the most widely used tools for multi-chain portfolio tracking and tax calculation in 2026. These pair well with ChainAware’s behavioral analytics layer.

ChainAware.ai — Complete On-Chain Intelligence Suite

Wallet Auditor. Credit Score. Prediction MCP.

Understand your risk profile, build a credit history from your on-chain behavior, and access AI-powered wallet intelligence. Free to start. No KYC. Covers 8 networks.

Frequently Asked Questions

How many assets should I hold in a diversified crypto portfolio?

Markowitz optimization typically converges on 5-10 positions for a maximum Sharpe ratio portfolio. More positions often add correlation without meaningful risk reduction. Focus on assets with genuinely different correlation profiles rather than maximizing position count.

What percentage should Bitcoin be in a crypto portfolio?

For most investors, Bitcoin + Ethereum together should represent 40-60% of a crypto portfolio. Bitcoin provides stability, liquidity, and serves as the market’s benchmark asset. Higher allocations (60-80%) suit conservative investors; lower allocations suit those with longer time horizons and higher risk tolerance who want more altcoin exposure.

Should I include stablecoins in my portfolio?

Yes — a 10-20% stablecoin allocation has two benefits in an MPT framework. It reduces portfolio volatility (stablecoins have near-zero correlation to crypto) and provides dry powder to buy dips. Deployed in high-quality DeFi money markets, stablecoins can also generate 4-8% APY yield with minimal risk.

What is the Efficient Frontier in crypto?

The Efficient Frontier is the set of portfolios that offer the maximum possible expected return for any given level of risk, or equivalently the minimum risk for any given expected return. Portfolios below the frontier are suboptimal — you could get better risk-adjusted returns by reallocating. Markowitz optimization computes the frontier using expected returns, volatilities, and correlations for all available assets.

How does a crypto credit score relate to portfolio management?

Your on-chain credit score (from the ChainAware Wallet Auditor) reflects your portfolio management behavior: consistency, diversification, cash flow management, and fraud risk. A high credit score unlocks undercollateralized lending — allowing you to borrow capital against your portfolio without locking up excess collateral, which improves your overall capital efficiency as an investor.

How often should I rebalance my crypto portfolio?

Quarterly calendar rebalancing is a practical baseline for most investors. Consider also setting a 5 percentage point drift threshold — rebalance at your quarterly review only if an asset has moved more than 5 points from its target weight. This minimizes transaction costs and tax events while keeping your allocation meaningfully on-target.

What tools can help me optimize my crypto portfolio?

Python’s pypfopt library implements full Markowitz optimization for custom portfolios. CoinGecko Portfolio and Koinly handle multi-chain tracking and tax calculation. ChainAware’s Prediction MCP adds behavioral wallet intelligence to AI-powered portfolio tools. For the full ChainAware product ecosystem, see the complete product guide.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or professional advice. Cryptocurrency markets are highly volatile. Do not invest more than you can afford to lose. Consult a qualified financial advisor before making investment decisions.