Credit scoring has been the backbone of traditional finance for decades. It determines who gets a mortgage, what interest rate a small business pays, and whether a student can access education financing. The global consumer lending market exceeded $11 trillion in 2025 — and virtually every dollar of it was allocated based on credit scores.

In Web3, credit scoring has been almost entirely absent. Not because it isn’t needed — but because DeFi solved the credit risk problem in a blunter way: require borrowers to put up more collateral than they borrow. If they can’t repay, the protocol liquidates their collateral. No credit assessment needed.

This worked. But it created a profound paradox: if you already have the assets, why do you need to borrow? Overcollateralized DeFi lending serves a narrow use case and excludes the majority of potential borrowers worldwide.

ChainAware Credit Score changes this. It’s a Web3-native credit scoring system built on three pillars: the Wallet Auditor (behavioral profile), the Fraud Detector (98% AI accuracy), and Cash Flow Analysis. Together they generate a score from 0 to 1000 that works without KYC, without identity verification, and without any off-chain data — purely from on-chain behavior.

This guide explains how TradFi credit scoring works, why DeFi didn’t need it until now, what ChainAware’s system actually does, and the surprising use cases for Web3 credit scoring beyond lending.

What Is Credit Scoring in Traditional Finance?

Before understanding why Web3 credit scoring matters, it helps to understand exactly what TradFi credit scoring does — and why it works so well.

A credit score is a number that represents how likely you are to repay a debt. In the United States, the dominant standard is the FICO score, ranging from 300 to 850, used by 90% of top lenders to make lending decisions. In Europe and elsewhere, equivalent systems exist under different names but the same logic.

FICO scores are calculated from five factors: payment history (35% — have you paid on time?), amounts owed (30% — how much debt do you carry?), length of credit history (15% — how long have you been a borrower?), new credit (10% — have you recently applied for multiple new accounts?), and credit mix (10% — do you manage different types of credit responsibly?).

The score determines three things that matter enormously: whether you get approved for credit at all, what interest rate you pay (a 100-point score difference can mean thousands of dollars in interest over a loan’s lifetime), and how much you can borrow.

Why Traditional Credit Scoring Works

The system works because of four interlocking features. First, identity is verified — lenders know exactly who they’re lending to through government IDs, social security numbers, and KYC processes. Second, legal recourse exists — a defaulting borrower can be sued, have wages garnished, and face asset seizure. Third, credit history is centralized — bureaus like Experian, Equifax, and TransUnion maintain comprehensive records that follow individuals for years. Fourth, consequences are real — a damaged credit score affects housing, employment, and financial opportunity for a decade.

This combination of verified identity, legal enforceability, centralized history, and durable consequences keeps default rates for personal loans at 2–5% — remarkably low for often-unsecured or lightly-secured credit. According to the Consumer Financial Protection Bureau, credit scoring has enabled the modern credit economy — allowing billions of people to buy homes, start businesses, and access education without having the full purchase price upfront.

AI-Powered Web3 Credit — No KYC Required

Check Your Wallet Credit Score — Free

ChainAware Credit Score analyzes your on-chain behavioral history — Wallet Auditor + Fraud Detector + Cash Flow — and generates a 0–1000 credit score. No personal data. No KYC. Real-time. Free.

The DeFi Paradox: Why Credit Scoring Wasn’t Needed

DeFi’s approach to lending is radically different from TradFi — and the difference reveals why credit scoring hasn’t been needed until now.

Protocols like Aave, Compound, and MakerDAO revolutionized lending by removing banks and intermediaries entirely. Anyone with crypto assets could borrow against them instantly, without approval, without a bank account, without credit history. This was genuinely revolutionary access to financial services.

But there was a catch: DeFi borrowing is overcollateralized. To borrow $10,000, you must lock up $15,000–$20,000 in collateral — typically 150–200% of the loan amount. If your collateral value falls below the required threshold (because the crypto market drops), the protocol automatically liquidates your position. You don’t need a credit score because the protocol doesn’t need to trust you — it’s already holding more than it lent you.

This solved the core problem elegantly: in a pseudonymous blockchain environment with no legal recourse, overcollateralization made lending trustless and safe. But it created a different problem.

Overcollateralization: The Blunt Solution and Its Limits

The overcollateralization model works — but it’s massively capital-inefficient and excludes most potential borrowers from the global population.

Consider the paradox: if you already hold $15,000 in crypto assets, why do you need to borrow $10,000? The use cases are real but narrow — mostly tax optimization (avoid selling assets and triggering capital gains), or leveraged yield strategies where you borrow stablecoins against ETH to earn yield on both. These are legitimate DeFi strategies, but they’re available only to people who already have significant crypto holdings.

The global population that could benefit from credit — people who need capital to start businesses, fund education, cover cash flow gaps, or access financial services for the first time — is almost entirely excluded from DeFi lending because they don’t have the collateral to unlock it.

According to research on undercollateralized DeFi lending, effective credit scoring systems could unlock trillions of dollars in previously inaccessible lending markets. The capital efficiency problem is the single biggest constraint on DeFi’s growth trajectory.

There are also structural limitations beyond individual borrowers. DAOs need working capital for operations but often can’t overcollateralize without selling governance tokens. Web3 businesses need supplier credit and net payment terms. NFT creators need financing against future royalties. None of these fit the overcollateralized model.

The 2026 Shift: When Credit Scoring Becomes Essential

In 2026, several forces are converging to make on-chain credit scoring not just useful but necessary.

DeFi maturation has brought protocols like Goldfinch, TrueFi, and Credix to the point where undercollateralized lending is demonstrably viable — if you have the risk assessment infrastructure to support it. The question is no longer whether undercollateralized DeFi lending can work, but whether credit scoring tools are good enough to make it work safely at scale.

Institutional involvement has changed the standard of care. Traditional finance institutions entering Web3 expect credit scoring infrastructure — they won’t lend without risk assessment tools that meet at least the basic standards they apply in TradFi.

Real-World Asset (RWA) integration is growing rapidly. Tokenized real-world assets require credit assessment for efficient capital allocation. You can’t overcollateralize a business loan with 200% of the company’s value.

AI advancement has made behavioral analysis at scale viable. The models that power ChainAware’s credit scoring system — trained on millions of confirmed wallet profiles across 8 blockchains — achieve 98% accuracy in predicting behavior. The technical capability now matches the need.

Build Credit-Aware Applications

Prediction MCP: Real-Time Credit Intelligence for AI Agents

The Prediction MCP gives your AI agents and backend systems direct access to ChainAware’s credit scores, fraud probabilities, wallet behavioral profiles, and predicted intentions — in real time. Build autonomous lending agents, risk management systems, and personalized DeFi experiences.

Web3 Credit Score Use Cases Beyond Lending

The most obvious application of Web3 credit scoring is undercollateralized lending — but it’s far from the only one. In 2026, credit scores are becoming useful infrastructure across a wide range of Web3 contexts.

User Acquisition Quality and Marketing Efficiency

Web3 projects spend millions on marketing and can’t distinguish between genuine users and bots, wash traders, or airdrop farmers. A credit score provides an immediate quality signal: high-score wallets are experienced, legitimate DeFi participants. Low-score wallets are often auto-generated, short-lived, or bot-operated.

Projects using Web3 Behavioral Analytics with credit score integration can target marketing to genuine high-quality users, tier incentives based on wallet quality, and dramatically reduce the cost of acquiring users who will actually engage with and transact on the platform. As documented in our analysis of Web3 marketing effectiveness, the gap between genuine users and low-quality traffic is one of the biggest efficiency drains in DeFi growth marketing.

Airdrop Screening and Fair Token Distribution

Airdrop farming — creating thousands of wallets to claim token distributions — costs projects enormous amounts of value that never reaches genuine community members. Credit score screening of airdrop recipients distinguishes genuine, experienced DeFi users (high score, rich on-chain history) from auto-generated farming wallets (near-zero score, no real history) before tokens are distributed.

DAO Treasury Credit Lines

DAOs often need working capital for development, operations, or strategic investments but lack the liquid crypto assets to overcollateralize efficiently without selling governance tokens. A DAO treasury address with consistent on-chain revenue, diversified holdings, and a strong behavioral profile can qualify for credit-based financing — working capital without the token dilution of a fundraise or the capital inefficiency of overcollateralization.

NFT Creator Financing

Creators with consistent NFT sales histories, high royalty generation, and strong collector networks can access advance financing against future royalties. Their on-chain track record provides the credit history; the Wallet Auditor provides the risk profile; the Fraud Detector validates behavioral legitimacy. A creator who has successfully launched three collections with 95%+ sell-through rates has a demonstrable credit profile that supports lending — without any KYC.

B2B Web3 Transactions and Net Payment Terms

Web3 businesses that transact with pseudonymous counterparties face trust barriers that slow business development. Credit scores enable net payment terms, supplier financing, and partnership vetting based on verifiable on-chain behavior rather than reputation claims that can’t be verified. Before sending a large advance payment to a service provider, checking their wallet’s credit score via the Wallet Auditor provides behavioral verification that no other tool can offer.

Gaming and Metaverse Anti-Bot Measures

Play-to-earn and GameFi platforms are systematically exploited by bot farms that drain rewards designed for genuine players. Credit scores distinguish real players (with diverse on-chain histories, genuine asset management behavior, and established wallet ages) from bot wallets (new, narrow, pattern-repeating). Progressive rewards for high-score users and restrictions on low-score wallets protect the economics of play-to-earn ecosystems.

Insurance and Dynamic Premium Pricing

DeFi insurance protocols can use credit scores as risk indicators for dynamic premium pricing. A wallet with an excellent credit score and clean fraud history pays lower premiums for coverage than a high-risk wallet with suspicious behavioral patterns. This aligns incentives: good actors pay less, and the insurance pool’s risk is more accurately priced.

How ChainAware Credit Score Works: The Three Pillars

ChainAware’s credit scoring system is built on three data pillars that together provide a comprehensive picture of a wallet’s creditworthiness — entirely from on-chain behavior, with no off-chain data, no KYC, and no personal information.

Pillar 1: Wallet Auditor (40% Weight)

The Wallet Auditor provides the behavioral profile component of the credit score. It analyzes the wallet across five dimensions: Experience Level, Risk Willingness, Predicted Intentions, Wallet Rank, and AML Status. A wallet with high experience, moderate risk willingness, legitimate intentions, and a high Wallet Rank has the behavioral profile of a reliable borrower. For a complete breakdown, see the Wallet Auditor complete guide.

Pillar 2: Fraud Detector (35% Weight)

The Predictive Fraud Detector achieves 98% accuracy in identifying wallets likely to engage in fraudulent behavior — before it happens. For credit scoring purposes, this component is critical: a borrower who defaults is one risk, but a borrower who never intended to repay is a different and more serious risk. It generates a Trust Score that contributes directly to the credit assessment.

As documented in our transaction monitoring guide, fraud is frequently committed with clean funds — meaning AML checks alone are insufficient. The Fraud Detector’s behavioral approach catches risk that purely forensic tools miss.

Pillar 3: Cash Flow Analysis (25% Weight)

Cash flow patterns are the strongest direct indicator of repayment capacity. ChainAware’s AI models analyze income consistency, source diversity, growth trends, and liquidity management. A wallet with consistent income from multiple DeFi yield sources, maintained reserves, and disciplined liquidity management has demonstrably better repayment capacity than one with erratic cash flows and overleveraged positions.

The Credit Score Formula

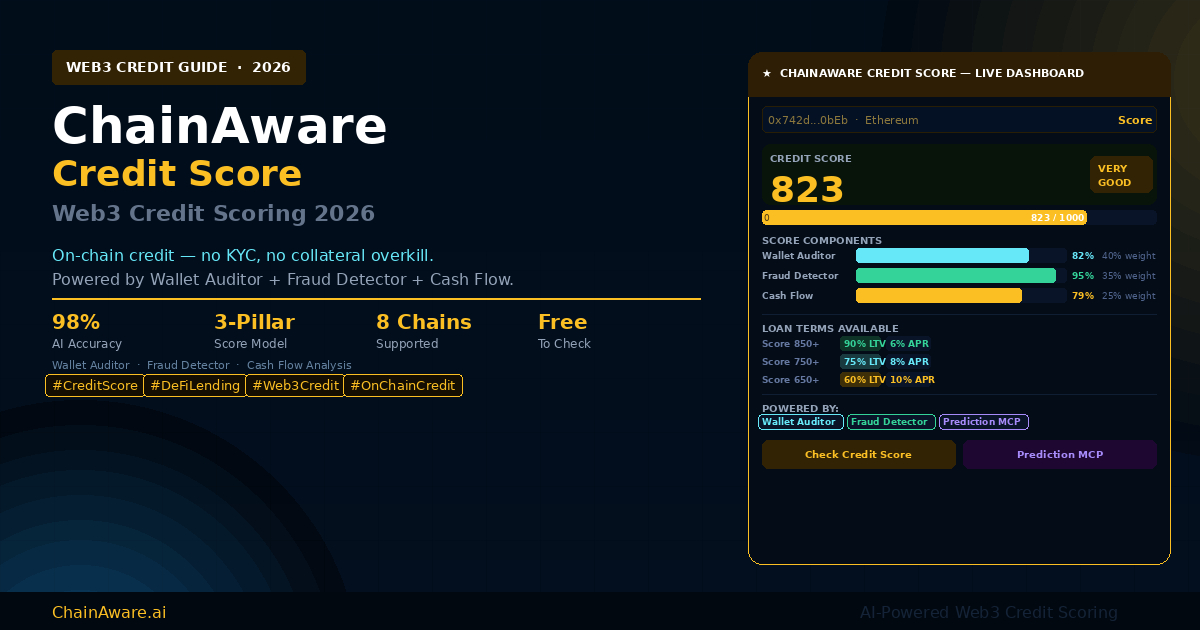

Credit Score = (Wallet Auditor × 0.40) + (Fraud Risk × 0.35) + (Cash Flow × 0.25)Unlike static credit reports that update monthly, ChainAware scores update continuously — every transaction can affect the score, and major behavioral changes trigger immediate recalculation.

Proven in Production — SmartCredit.io Case Study

43% More Borrowers. 68% Lower Default Rates.

ChainAware Credit Scores enabled dynamic LTV ratios on SmartCredit.io — 850+ scores at 90% LTV, 750+ at 75% LTV. Result: 43% more borrower acquisition, 68% lower defaults, and $2.3M in loan volume in the first 6 months. The Wallet Auditor is free to check for any wallet.

Score Ranges and What They Mean

850–1000: Excellent. Institutional-grade reliability. Long-established wallet with diverse protocol history, high Trust Score, consistent positive cash flows. Qualifies for 90%+ LTV lending with the lowest available interest rates.

750–849: Very Good. Proven track record of responsible on-chain behavior. Consistent DeFi participation, moderate to low fraud risk, solid cash flow patterns. Typical terms: 75% LTV, competitive APR.

650–749: Good. Solid history with minor risk factors. Active on-chain but with some behavioral signals worth monitoring. Typical terms: 60% LTV, moderate APR. Eligible for credit-based lending on most platforms.

550–649: Fair. Mixed history requiring monitoring. Limited experience, elevated risk signals, or inconsistent cash flows. May qualify for limited credit on specific platforms with stricter terms.

Below 550: Poor. High-risk behavioral profile. New wallets, suspicious patterns, poor cash flow, or elevated fraud probability fall here. Requires full overcollateralization on standard DeFi lending protocols.

How to Check Your Web3 Credit Score

Checking your credit score is straightforward and free. Visit the ChainAware Wallet Auditor, paste any wallet address, and select the network. Within seconds you receive your complete credit profile: overall Credit Score (0–1000), Wallet Auditor dimensions, Fraud Detector Trust Score, Cash Flow summary, and the loan terms you would qualify for on credit-enabled platforms.

The check covers 8 networks: Ethereum, BNB Chain, Base, Polygon, Haqq, Solana, TON, and Tron. For DeFi protocols and lenders wanting to integrate credit scoring into their platform, three integration paths are available: no-code via Google Tag Manager, REST API, and on-chain oracle feeds. For the complete product ecosystem overview, see the ChainAware complete product guide.

Prediction MCP: Credit Intelligence for AI Agents

The Prediction MCP makes ChainAware’s credit intelligence available programmatically to AI agents and backend systems. When a user connects their wallet, your AI agent queries the MCP with the wallet address and receives the complete credit profile — score, fraud probability, behavioral dimensions, and predicted intentions — in real time.

For DeFi platforms specifically, the Prediction MCP enables five high-impact credit applications: smarter LTV ratio assignment, automated yield strategy recommendations calibrated to risk profile, real-time position risk monitoring, personalized product suggestions matched to financial capacity, and proactive engagement timed to behavioral windows. See 5 ways Prediction MCP turbocharges DeFi platforms for the full breakdown.

How to Improve Your Web3 Credit Score

Unlike TradFi credit scores that change slowly over years, on-chain credit scores can improve meaningfully within weeks if behavior changes. For the Wallet Auditor component: build consistent transaction history, diversify your protocol footprint, increase wallet age and activity continuity. For the Fraud Detector component: avoid any activity that resembles fraud preparation — mixer services, coordinated wallet interactions, or wash trading patterns. For the Cash Flow component: demonstrate consistent on-chain income, maintain meaningful reserves, and manage leverage conservatively.

Most users see demonstrable score improvement within 30 days of behavioral changes, meaningful improvement within 90 days, and potential band advancement within 6 months of sustained consistent behavior. The Wallet Rank complete guide explains exactly what drives rank improvement.

ChainAware.ai — Complete Web3 Credit Infrastructure

Credit Score · Fraud Detector · Prediction MCP

AI-powered credit scoring built on Wallet Auditor + Fraud Detector + Cash Flow Analysis. Check any wallet in seconds. No KYC. No personal data. Covers 8 networks. Free to start.

Frequently Asked Questions

What is a credit score in crypto?

A crypto credit score is a numerical assessment of a wallet’s creditworthiness based purely on on-chain behavioral data — transaction history, protocol interactions, cash flows, and fraud risk signals. It works without KYC, without personal data, and without centralized credit bureaus. ChainAware’s score ranges from 0 to 1000, combining Wallet Auditor (40%), Fraud Detector (35%), and Cash Flow Analysis (25%).

Why hasn’t credit scoring been widely used in DeFi until now?

DeFi lending has historically required overcollateralization — borrowers lock up 150–200% of the loan value as collateral. This eliminated the need for credit assessment entirely. But overcollateralization is capital-inefficient, excludes most potential borrowers, and can’t serve use cases like DAO treasury credit, creator financing, or undercollateralized lending. Credit scoring unlocks these use cases.

How is ChainAware’s credit score different from FICO?

FICO uses centralized credit bureau data tied to a verified identity. ChainAware uses on-chain behavioral data from a wallet address — no identity verification, no personal information, no credit bureau. FICO updates monthly; ChainAware updates in real time with every transaction. FICO requires a social security number; ChainAware requires only a wallet address.

Does checking my credit score affect it?

No. Looking up a wallet’s credit score is a read-only operation with no effect on the score itself. Only actual on-chain behavior affects the score.

Can I have different scores for different wallets?

Yes — each wallet has its own independent credit score based on its specific activity. If wallets demonstrate sybil-like patterns (coordinated behavior suggesting single-entity control of multiple wallets), this may negatively affect scores across related wallets.

What’s the minimum score needed for undercollateralized lending?

Most credit-enabled lending protocols require a minimum score of 650. Scores of 750+ typically qualify for 75% LTV. Scores of 850+ may qualify for 90%+ LTV on supported platforms. Below 550, full overcollateralization is typically required.

Can AI agents query credit scores automatically?

Yes. The Prediction MCP provides programmatic access to credit scores, fraud probabilities, behavioral profiles, and predicted intentions via API. AI agents can query it in real time for autonomous lending decisions, risk monitoring, and personalized user experiences.

Which blockchains are supported?

Ethereum, BNB Chain, Base, Polygon, Haqq, Solana, TON, and Tron — covering the majority of active DeFi activity in Web3.