This DeFi credit score comparison covers seven platforms tackling one of DeFi’s most important unsolved problems: assessing borrower risk without KYC, without identity, using only public blockchain data. Today, over 90% of DeFi loans are overcollateralized. Borrowers deposit $150 to access $100 — a pawnshop model that limits how much capital DeFi can unlock. On-chain credit scoring is the missing piece.

Several platforms have tackled this problem seriously. Each one takes a different approach — different data sources, different scoring methods, different chain coverage, and different integration models. In this comparison, we evaluate seven platforms across every dimension that matters: scoring methodology, chain coverage, fraud integration, KYC requirements, integration model, output format, and real strengths and weaknesses.

In This Article

- Why DeFi Credit Score Infrastructure Matters in 2026

- The Problem No DeFi Credit Score Addresses — Except One

- ChainAware — Fraud-Integrated Borrower Risk Grading

- Cred Protocol — Protocol-Side Passive Scoring

- Spectral Finance — The MACRO Score

- RociFi — NFT-Based Credit Identity

- Masa Finance — Data Sovereignty Approach

- TrueFi — The OG Uncollateralized Lender

- Maple Finance — Institutional Credit Market

- Providence (Andre Cronje) — Scale-First Approach

- Full DeFi Credit Score Comparison Table

- How to Choose the Right Platform

- FAQ

Why DeFi Credit Score Infrastructure Matters in 2026

The global unsecured lending market is worth approximately $11 trillion according to TrueFi’s analysis. Virtually none of it flows through DeFi today. The reason is structural: without creditworthiness assessment, protocols must require overcollateralization. Borrowers prove they don’t need the loan by posting more than they borrow. It’s circular, capital-inefficient, and excludes most people who could benefit from decentralized credit.

On-chain credit scoring changes this dynamic entirely. Every DeFi interaction — borrowing, repayment, liquidation avoidance, protocol choice, asset management — leaves a permanent, verifiable record on the blockchain. A wallet that managed leveraged positions across Aave and Compound for three years without liquidation is clearly more creditworthy than a wallet created last week. The data already exists. The question is what methodology turns it into a reliable credit signal.

According to DeFiLlama, DeFi lending TVL exceeded $50 billion in 2025. Furthermore, industry research puts the overcollateralized share of all DeFi loans above 90%. That means the vast majority of capital sits locked in inefficient mechanics. Consequently, platforms that crack undercollateralized lending at scale will capture an enormous share of the next wave of DeFi growth.

The Problem No DeFi Credit Score Addresses — Except One

Every DeFi credit scoring platform asks one question: “Has this borrower managed debt responsibly?” That is necessary, but it’s not sufficient. None of these platforms — with one exception — asks the equally critical question: “Is this borrower going to commit fraud?”

In traditional finance, fraud and credit risk are separate problems. Banks have legal recourse, account freezes, and clawback mechanisms. A fraudulent borrower causes damage that is catastrophic but recoverable. In DeFi, however, blockchain transactions are permanent. A fraudster who receives an undercollateralized loan and drains it causes immediate, unrecoverable damage. No credit history analysis catches a wallet with a spotless repayment record and a fraud probability of 0.85.

This structural gap separates ChainAware from every other platform in this comparison. ChainAware integrates fraud probability as a core signal — not a separate tool, but 40% of the scoring formula. For any lending protocol, this distinction is critical. It determines whether the credit score tells you who repaid in the past, or who is actually safe to lend to right now. For more context, see our analysis of AML screening vs predictive fraud detection.

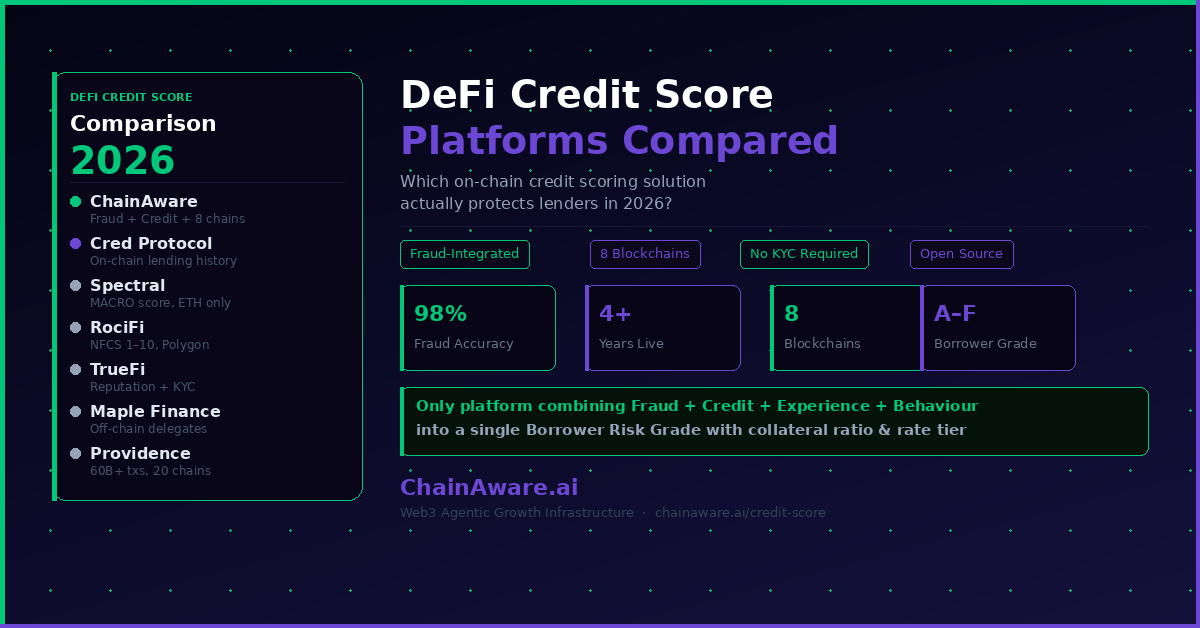

ChainAware — Fraud-Integrated Borrower Risk Grading

Website: chainaware.ai/credit-score

Model age: 4+ years in production

Chain coverage (Lending Risk Assessor): ETH, BNB, POLYGON, TON, BASE, TRON, HAQQ, SOLANA

Chain coverage (Credit Score API): ETH only

KYC required: No

Two Layers: Credit Score API and Lending Risk Assessor

ChainAware’s credit scoring product has two distinct layers. Understanding both separately is important before integrating.

The first layer is the raw Credit Score API — available on Ethereum only. It produces a riskRating from 1–9 by combining on-chain transaction history with social graph analysis. Think of it as a FICO score for DeFi wallets. ChainAware originally developed this model for SmartCredit.io’s lending platform, and it has run in production for more than four years. Anyone can check any ETH wallet for free at chainaware.ai/credit-score.

The second — and more powerful — layer is the Lending Risk Assessor agent. This open-source MIT-licensed agent is available on GitHub. It works on 8 blockchains and combines four signals into a single Borrower Risk Score (BRS) on a 0–100 scale:

| Component | Weight | Source | Chains |

|---|---|---|---|

| Fraud Probability | 40% | predictive_fraud MCP tool | ETH, BNB, POLYGON, TON, BASE, TRON, HAQQ |

| Credit Score | 20% | credit_score MCP tool | ETH only (defaults to 50 on other chains) |

| On-chain Experience | 25% | predictive_behaviour MCP tool | ETH, BNB, BASE, HAQQ, SOLANA |

| Behavioural Profile | 15% | predictive_behaviour MCP tool | ETH, BNB, BASE, HAQQ, SOLANA |

Actionable Output: Grade, Collateral Ratio, Rate Tier, LTV

The BRS maps directly to a Grade A–F. Each grade then translates into a recommended collateral ratio, interest rate tier, and LTV limit. In other words, a lending protocol receives a complete lending decision — not just a score to interpret manually. Hard rejection rules apply before any scoring begins: wallets with fraud probability above 0.70, confirmed fraud status, or AML forensic flags are automatically declined regardless of credit history.

ChainAware’s key advantages over every other platform in this comparison are:

- Only platform with fraud integration — 40% of the BRS comes from predictive fraud probability, catching the risk that credit history alone misses

- Oldest production model — 4+ years live, continuously retrained, with a paying enterprise client base from day one

- Complete lending decision — grade, collateral ratio, rate tier, LTV, and secondary risk flags in one response

- 8-chain risk assessment — broadest coverage, with full credit score on ETH

- Open-source agent — MIT-licensed, composable with 30 other ChainAware agents

- Beyond lending — also powers ABC client filtering, growth targeting, and collateral decisions

- Zero borrower action needed — the protocol calls the API with any wallet address; the borrower does nothing

For the full methodology, see the complete Web3 credit scoring guide and the Credit Scoring Agent guide. For compliance integration, see our complete KYT and AML guide for DeFi.

Check Any Wallet’s Credit Score — Free

ChainAware Credit Score — 4+ Years Live, ETH Wallets, Instant

The oldest production DeFi credit model. Check any Ethereum wallet instantly — riskRating 1–9, fraud probability, behavioral profile, full borrower risk assessment. Free individual checks. No signup required. API access for lending protocols.

Cred Protocol — Protocol-Side Passive Scoring

Website: credprotocol.com

Chain coverage: Ethereum-focused, expanding

KYC required: No

Cred Protocol is ChainAware’s closest structural competitor. Both are API-first and protocol-facing, and both have shipped MCP endpoints for AI agent integration. Cred focuses on on-chain lending history as its primary scoring signal — specifically debt-to-collateral ratios, liquidation history, and repayment patterns across Aave, Compound, and MakerDAO.

Cred’s genuine USP: Passive protocol-side scoring done cleanly. Lenders integrate once via API, and all borrowers receive scores automatically — no borrower action required. Additionally, Cred has shipped live MCP endpoints and a unified agent skill file, giving it serious AI agent integration credentials. Developers also benefit from a free sandbox with unlimited testing before going to production.

ChainAware’s response: Cred scores lending history only. Consider a borrower with a spotless three-year Aave repayment record and a current fraud probability of 0.80. Cred would approve them for an undercollateralized loan. ChainAware would reject them immediately. Lending history tells you who repaid in the past; fraud probability tells you who intends to repay in the future. Both signals matter. Moreover, ChainAware offers 31 open-source agent definitions versus Cred’s single MCP skill file — a substantially deeper ecosystem for protocols building automated underwriting pipelines.

Spectral Finance — The MACRO Score

Website: spectral.finance

Chain coverage: Ethereum

KYC required: No

Spectral Finance introduced the MACRO score — Multi-Asset Credit Risk Oracle. It quantifies creditworthiness using on-chain transaction data across multiple DeFi protocols. MACRO is the most academically cited on-chain credit score in the space, and Spectral has built strong brand recognition around capital efficiency and quantitative rigor.

Spectral’s genuine USP: Academic credibility and developer recognition. MACRO carries a well-documented, research-grounded methodology. For protocols that want a credit scoring solution with independent citations and analysis behind it, Spectral brings meaningful weight. They’ve also built tooling around the score rather than just producing a number.

ChainAware’s response: MACRO runs on ETH only and outputs a number — not a lending decision. A protocol integrating MACRO still needs to define collateral requirements, interest rates, and LTV limits itself. By contrast, ChainAware’s Lending Risk Assessor returns the complete decision: Grade A–F, collateral ratio, rate tier, max LTV, and risk flags. Furthermore, MACRO has no fraud component — meaning it misses the risk that causes the most catastrophic outcomes in undercollateralized DeFi lending.

RociFi — NFT-Based Credit Identity

Website: rocifi.xyz

Chain coverage: Polygon

KYC required: No

Funding: $2.7M seed round

RociFi introduced one of the most conceptually innovative approaches in this comparison. Its Non-Fungible Credit Score (NFCS) is a non-transferable NFT that ties on-chain credit identity to a specific wallet. Scores range from 1–10 (lower = lower risk) and use machine learning on Polygon lending history. Crucially, burning the NFCS to escape a bad score means losing all accumulated credit history — creating real reputational consequences for default.

RociFi’s genuine USP: Persistent on-chain credit identity with genuine default consequences. By making credit history non-transferable, RociFi introduces an economic deterrent that purely algorithmic systems lack. The identity model is novel and ahead of the field conceptually.

ChainAware’s response: The NFCS requires borrower opt-in. The wallet must mint the token and commit its address. As a result, only self-selected borrowers participate — creating selection bias, since those who opt in likely have favorable profiles. ChainAware, by contrast, requires zero borrower action. The lending protocol calls the API with any wallet address and gets an instant assessment. Additionally, RociFi is Polygon-only and has shown limited on-chain activity since 2023, which raises questions about ongoing development.

Masa Finance — Data Sovereignty Approach

Website: masa.finance

Chain coverage: Multi-chain

KYC required: No (on-chain data), optional off-chain data

Funding: $3.5M pre-seed

Masa Finance approaches credit scoring from a data sovereignty angle. Users own their financial data and choose who to share it with. The platform combines on-chain transaction history with optional off-chain social and financial data. Users can also monetize their anonymized data through token rewards.

Masa’s genuine USP: Data ownership resonates strongly with a Web3 audience aligned with self-sovereignty. The combination of on-chain and off-chain data gives Masa a richer signal set than pure on-chain approaches — for users who choose to share. Multi-chain coverage is also broader than most competitors.

ChainAware’s response: User-controlled data sharing creates a fundamental problem — borrowers can share favorable data and withhold unfavorable data. This produces systematic upward bias in scores. ChainAware uses only public blockchain data that no borrower can manipulate or selectively disclose. As a result, the score is objective and consistent. For protocols that require reliable, unbiased risk assessment, the public-data-only approach is simply more dependable.

Integrate DeFi Credit Scoring + Fraud Detection via MCP

ChainAware Lending Risk Assessor — Grade A–F on 8 Blockchains

The only borrower risk assessment combining fraud probability (40%), credit score (20%), experience (25%), and behavioural profile (15%) into a single Grade A–F with collateral ratio, rate tier, and LTV. ETH, BNB, BASE, POLYGON, TON, TRON, HAQQ, SOLANA. MIT-licensed agent on GitHub.

TrueFi — The OG Uncollateralized Lender

Website: truefi.io

Chain coverage: Ethereum

KYC required: Yes — off-chain onboarding

Launch: November 2020

TrueFi is the most battle-tested platform in this comparison. It has originated uncollateralized loans at institutional scale and has real repayment history to show for it. The model combines on-chain analytics with off-chain KYC and a legally-binding loan agreement. TRU token holders vote to approve or deny specific borrower terms. Moreover, borrowers face genuine legal recourse on default — something no purely on-chain system can replicate.

TrueFi’s genuine USP: The longest track record of actual uncollateralized loan origination in DeFi. TrueFi has proven the model works — loans were issued, repaid, and defaults resolved through legal processes. For lenders who want a battle-tested system with institutional-grade risk management, TrueFi’s history carries real weight.

ChainAware’s response: TrueFi’s KYC and off-chain onboarding requirements contradict the permissionless ethos of DeFi. They create geographic, identity, and regulatory barriers that exclude most potential borrowers. Additionally, TrueFi is borrower-facing — you apply for a loan. ChainAware is lender-facing — the protocol screens any wallet automatically. For DeFi protocols serving anonymous wallets at scale, TrueFi’s architecture simply doesn’t fit the use case.

Maple Finance — Institutional Credit Market

Website: maple.finance

Chain coverage: Ethereum

KYC required: Yes — institutional borrowers only

Maple Finance targets a fundamentally different market. Rather than anonymous retail borrowers, Maple serves institutional clients — crypto market makers, trading firms, and corporate entities. Pool delegates, who are experienced credit professionals, perform manual due diligence on each borrower before approving loan terms.

Maple’s genuine USP: Institutional-grade underwriting with real human judgment. For large loans to known corporate entities, Maple’s pool delegate model brings genuine expertise. Delegates stake their own capital and reputation on each credit decision. No algorithm replicates the nuanced judgment of an experienced professional reviewing a company’s financials and market position.

ChainAware’s response: Pool delegate underwriting does not scale to retail DeFi. It makes economic sense for a $5M loan to a known market maker. It does not make sense for hundreds of anonymous wallets seeking $500–$5,000 in undercollateralized credit. Furthermore, Maple cannot assess anonymous wallet addresses at all — it requires identified legal entities. ChainAware handles exactly the opposite use case: automated, real-time, anonymous, scalable assessment of any wallet on any supported chain.

Providence (Andre Cronje) — Scale-First Approach

Creator: Andre Cronje (Yearn, Fantom/Sonic, Keep3r)

Chain coverage: 20 blockchain protocols

KYC required: No

Providence is Andre Cronje’s approach to on-chain credit scoring. It analyzes more than 60 billion transactions, 15 million loans, and over 1 billion wallets across 20 blockchain protocols. Importantly, scores tie to wallet addresses rather than persons — preserving privacy and self-sovereignty with no KYC required.

Providence’s genuine USP: Sheer data scale. At 60B+ transactions and 1B+ wallets, Providence has by far the largest dataset of any platform here. Broader data generally produces more robust pattern recognition, especially for edge cases. Additionally, Cronje’s credibility as the builder of Yearn, Fantom, and Sonic lends Providence significant weight among DeFi developers who trust his technical judgment.

ChainAware’s response: Providence targets borrowers checking their own score — not lending protocols automating borrower screening. As a result, protocols can only assess borrowers who proactively present their Providence score. This creates the same selection bias problem as RociFi. ChainAware, in contrast, assesses any wallet automatically without any borrower action. Moreover, Providence has no fraud component — the same structural gap that affects every other platform in this comparison. Finally, Cronje’s track record, while impressive, includes several abandoned projects, which creates uncertainty about long-term maintenance.

Full DeFi Credit Score Comparison Table

| Platform | Score Methodology | Chains | Fraud Integrated | KYC Required | Output Format | Integration Model | Open Source Agent | Model Age |

|---|---|---|---|---|---|---|---|---|

| ChainAware | Predictive ML: fraud (40%) + credit (20%) + experience (25%) + behaviour (15%) | 8 chains (risk assessor) + ETH (credit score) | ✅ Core signal (40%) | ❌ No | Grade A–F + collateral ratio + rate tier + LTV + flags | MCP + REST API, protocol-side automatic | ✅ MIT licensed | 4+ years |

| Cred Protocol | On-chain lending history, debt-to-collateral ratios | ETH-focused | ❌ No | ❌ No | Credit score + reports + alerts | MCP + API, protocol-side | Partial (MCP skill) | ~3 years |

| Spectral Finance | MACRO score — multi-asset on-chain tx data | ETH | ❌ No | ❌ No | MACRO numeric score | API | ❌ No | ~3 years |

| RociFi | ML on on-chain lending history, NFCS NFT | Polygon | ❌ No | ❌ No | NFCS score 1–10 | Borrower opt-in NFT | ❌ No | ~3 years |

| Masa Finance | On-chain + optional off-chain social data | Multi-chain | ❌ No | ❌ Optional | Decentralized credit score | User-controlled data sharing | ❌ No | ~3 years |

| TrueFi | Reputation + off-chain KYC + TRU governance vote | ETH | ❌ No | ✅ Yes | Approval/denial + loan terms | Borrower application + off-chain review | ❌ No | ~5 years (OG) |

| Maple Finance | Off-chain due diligence by pool delegates | ETH | ❌ No | ✅ Yes (institutional) | Pool delegate decision | Borrower application + manual review | ❌ No | ~3 years |

| Providence | Historical tx analysis, 60B+ transactions | 20 chains | ❌ No | ❌ No | Credit score tied to wallet | Borrower self-service check | ❌ No | ~2 years |

How to Choose the Right DeFi Credit Score Platform

The best choice depends on what you are building and where your primary risk lies.

Building a retail DeFi lending protocol for anonymous wallets?

ChainAware is the strongest option here. It requires zero borrower action, runs on 8 chains, returns a complete lending decision, and is the only platform that accounts for fraud. The open-source Lending Risk Assessor deploys in minutes via the Prediction MCP server. For ETH-only protocols wanting additional signal depth, combining ChainAware’s BRS with Cred Protocol’s lending-history data is a viable dual-signal approach.

Building on Ethereum and need academic credibility?

Spectral Finance’s MACRO score carries strong research credentials. It works well as a secondary signal in a multi-factor underwriting pipeline. Combine it with ChainAware’s fraud probability for a more complete picture than either provides alone.

Building for large institutional borrowers?

Maple Finance is purpose-built for this use case. The pool delegate model fits when loan sizes justify manual review and borrowers are identifiable entities. For compliance on top of institutional lending, ChainAware’s AML and transaction monitoring tools integrate well alongside it — see our AML integration guide for DApps.

Prioritizing user data sovereignty?

Masa Finance or RociFi suit this positioning well. However, keep the selection bias implications of borrower-controlled data in mind before committing to either.

Wanting the largest possible raw dataset?

Providence’s 60B+ transaction dataset is the largest foundation in the space. It is valuable for research and analysis. For automated real-time protocol-side underwriting, however, confirm API accessibility and integration model before treating it as a production dependency.

For a broader view of how credit scoring fits into the full DeFi security and growth stack, see our guides on 5 ways the Prediction MCP turbocharges DeFi platforms, real AI use cases for Web3 projects, and why 90% of connected wallets never transact.

Build Automated Underwriting with 31 Open-Source Agents

ChainAware Prediction MCP — Credit, Fraud, AML, Behaviour in One API

Connect any MCP-compatible AI agent to ChainAware’s full intelligence stack: credit scoring, fraud detection, rug pull detection, AML screening, and behavioral profiling. 31 MIT-licensed agent definitions on GitHub. ETH, BNB, BASE, POLYGON, TON, TRON, HAQQ, SOLANA. API key required.

Frequently Asked Questions

What is a DeFi credit score and how does it differ from a FICO score?

A traditional FICO score uses identity-linked financial records held by centralized bureaus — credit card history, debt levels, account age. A DeFi credit score uses public on-chain transaction data — wallet addresses, protocol interactions, repayment behavior in DeFi lending — with no identity linkage and no central custodian. The goal is the same: predict creditworthiness. The data source, methodology, and privacy properties are completely different. DeFi credit scores work on pseudonymous wallets without any personal information.

Why does ChainAware’s credit score only work on ETH while the Lending Risk Assessor covers 8 chains?

The raw credit_score API combines on-chain transaction history with social graph analysis and was built specifically for Ethereum. The Lending Risk Assessor works on 8 chains because it uses a composite formula. Fraud probability covers 7 chains. On-chain experience and behavioral profile cover 5 chains. The credit score applies on ETH and defaults to a neutral 50 on other chains. The result is a complete borrower risk grade on 8 chains, with the full credit score contributing on ETH and conservative defaults elsewhere. The agent flags this limitation clearly in every output.

Why does ChainAware include fraud probability in a DeFi credit score?

Because DeFi lending transactions are irreversible. In traditional finance, fraud detection after the fact still allows recovery — prosecution, clawbacks, account freezes. None of those mechanisms exist in DeFi. A borrower who fraudulently defaults on an undercollateralized loan causes immediate, permanent damage. A credit score based only on repayment history tells you who repaid in the past. It says nothing about who intends to repay in the future. ChainAware weights fraud probability at 40% precisely because it is the most consequential single risk signal for DeFi lending safety.

What is the Borrower Risk Score (BRS) formula?

BRS combines four components: fraud probability (40%), credit score (20%), experience (25%), and behaviour (15%). The fraud component equals (1 − probabilityFraud) × 100. The credit score component maps riskRating 1–9 to a 0–100 scale. The experience component uses the wallet’s experience score directly. The behaviour component assesses risk profile and protocol categories against lending-relevant patterns. The final BRS maps to grades A (85–100) through F (0–24), each with collateral ratios, rate tiers, and LTV limits. The complete methodology is in the open-source agent on GitHub.

Can ChainAware credit scoring be used outside of lending?

Yes — and this is one of ChainAware’s key differentiators. The credit score and borrower risk grade also power ABC client filtering (identifying your top 20% of highest-quality users), collateral decisions in DeFi protocols, growth targeting (prioritizing marketing spend toward high-creditworthiness wallets), and platform access tiering. No competitor offers this breadth from the same scoring infrastructure. See our Web3 behavioral user analytics guide for more on how behavioral profiling and credit scoring combine for growth use cases.

Is ChainAware’s credit score free to check?

Yes — any Ethereum wallet can be checked for free at chainaware.ai/credit-score. No signup is required. For API access and protocol integration, see chainaware.ai/pricing. The full Lending Risk Assessor agent is also free as an open-source MIT-licensed definition on GitHub, requiring only a ChainAware API key to run.

How does on-chain credit scoring handle wallets with no history?

New wallets are the hardest case for any credit scoring system. ChainAware’s Lending Risk Assessor caps new address grades at D regardless of other signals — insufficient history triggers conservative policy automatically. The agent flags new addresses and recommends reassessment after 90 days of on-chain activity. Most other platforms face the same cold-start limitation. In practice, undercollateralized lending only makes sense for wallets with established on-chain histories. New wallets should use standard overcollateralized products while they build history. See our Fraud Detector guide for how to handle new address assessment in the broader security stack.

The Only DeFi Credit Score With Fraud Integration

ChainAware.ai — Web3 Agentic Growth Infrastructure

Credit scoring + fraud detection + AML + behavioral profiling — all in one API. 4+ years live. 98% fraud accuracy. Grade A–F borrower assessment on 8 blockchains. Full credit score on ETH. 31 open-source agents on GitHub. Free individual wallet check. No KYC required.