Based on X Space #30 (two-part session) — ChainAware co-founders Martin and Tarmo. Watch the full recording on YouTube ↗ · Listen X-Space #30 X ↗

DeFi AI — the convergence of decentralized finance and artificial intelligence agents — is the topic of X Space #30. Martin and Tarmo, co-founders of ChainAware.ai and veterans of Credit Suisse’s private banking division, argue a straightforward thesis: AI will enter every existing Web3 domain and dramatically increase its utility. DeFi, with its 100% automated processes and freely accessible on-chain data, is the clearest example of where this transformation is already happening. This article covers the full two-part discussion — what DeFi AI actually means, why self-custody matters, what AI agents are doing in DeFi right now, and why the distinction between attention AI and real utility AI determines which projects survive.

In This Article

- The Core Thesis: AI Enters Every Web3 Domain

- Attention AI vs Real Utility AI — The Distinction That Matters

- What AI Agents Actually Are — and Two Types You Need to Know

- Self-Custody vs Custodial: Why DeFi Solves a Real Problem

- The MF Global Warning: Rehypothecation and Its Risks

- What DeFi AI Actually Means

- 1. Trading Agents — Pattern Recognition at Scale

- 2. Portfolio Management Agents — Risk-Adjusted Returns

- 3. Risk Monitoring Agents — Protecting Individual Positions

- 4. Marketing Agents — Behavioral Targeting for DeFi

- 5. Transaction Monitoring Agents — Address-Level Security

- 6. Credit Scoring Agents — Financial Ability Assessment

- SmartCredit: A Live Example of DeFi AI

- The Washing Machine Analogy: AI Frees Humans for Innovation

- Comparison: Attention AI vs Real Utility AI in DeFi

- FAQ

The Core Thesis: AI Enters Every Web3 Domain

The central hypothesis of X Space #30 is both simple and significant: AI is a megatrend that will penetrate every existing Web3 domain. It will not create new domains from scratch. Instead, it will enter gaming, NFTs, payments, DeFi, gambling, wallets, analytics, and every other category that already has real users and real utility — and it will make each one dramatically more effective.

Tarmo frames it precisely: “Existing domains have real use cases. AI is not there to invent new use cases. AI is there to improve the utility, to improve the value added of these existing domains even further.” The keyword is existing. Every domain that already generates revenue and serves real users becomes a candidate for AI-driven improvement. DeFi, with its fully automated processes and transparent on-chain data, is the most natural starting point.

Consequently, the term “DeFi AI” — or DeFAI as CoinGecko began categorizing it — represents an evolution, not a new invention. DeFi already has utility. AI makes that utility better. Furthermore, the same pattern will play out in every other Web3 category. There will be no separate “NFT AI” or “gaming AI” as distinct categories — there will simply be AI-enhanced versions of every category that already matters. For the broader context on how ChainAware approaches real utility AI, see our previous X Space discussion on attention AI vs real utility AI.

Attention AI vs Real Utility AI — The Distinction That Matters

Before diving into DeFi AI specifically, Martin and Tarmo revisit the framework they developed in X Space #29. Understanding this distinction matters because it separates projects worth building on from those that will disappear in the next market correction.

Attention AI — what Martin and Tarmo call “fake AI” in plain speech — generates narratives without generating utility. It combines impressive-sounding keywords: “tokenized decentralized AI optimization,” “cross-chain AI energy improvement,” “AI-driven supply chain healthcare.” These phrases attract retail investors because they sound sophisticated. However, behind them typically lies two or three lines of LLM prompts and a website. The product does not solve a specific, measurable problem for real users. As a result, when markets correct, attention AI projects are always the first to collapse.

Real utility AI, by contrast, uses proprietary machine learning models to solve specific, verifiable problems — and produces results that are measurable. ChainAware’s fraud detection achieves 98% accuracy, predicting future fraud before it occurs across 14M+ wallet profiles. That is a measurable claim. Moreover, it requires years of model development and training data that competitors cannot simply copy. This creates genuine competitive moats. For a detailed breakdown of what separates these two categories, see our complete guide to attention AI vs utility AI.

What AI Agents Actually Are — and Two Types You Need to Know

Tarmo defines AI agents with clarity that cuts through the hype: “AI agents are autonomous. They work 24 hours per day, seven days per week. No supervision — they just do it. They are self-running, self-healing, self-learning. They carry out tasks, measure results, and improve the next predictions continuously.”

Crucially, two fundamentally different types of AI agents exist — and confusing them leads to bad investment and integration decisions.

Type 1: LLM-Based Agents

LLM-based agents use large language models (ChatGPT, Claude, Gemini) to automate tasks through prompts. They are fast to build — sometimes just a few lines of prompt — and cover a wide range of use cases. Generating smart contract code, writing marketing copy, creating governance summaries — all of these suit LLM agents well. However, they have two critical limitations.

First, LLMs are statistical autoregression models. They predict the next most probable token in a sequence. They are linguistical models, not decision-making models. Feeding blockchain transaction data into an LLM and asking it to detect fraud produces unreliable results — because the LLM is optimized for language patterns, not for on-chain behavioral signals. Second, anyone can replicate an LLM-based agent quickly. There is no competitive moat. As a result, these agents commoditize rapidly.

Type 2: Predictive AI Agents

Predictive AI agents use proprietary ML models trained on specific data domains. Instead of predicting language sequences, they predict events and behaviors — will this wallet commit fraud, will this user borrow, will this contract rug pull? These models require substantial investment in data, training, and validation. Moreover, they produce measurable accuracy scores that can be backtested and verified. ChainAware’s fraud detection model, for example, achieves 98% accuracy — a number that is independently verifiable and has been validated over four years of production operation.

Tarmo explains the key difference in agent value: “The longer AI agents learn, they get superhuman performance. They go from junior to senior to master to principal to expert. When you let AI agents work and get continuously this feedback and relearn, relearn, relearn, then you will get super employees.” This continuous improvement loop is only possible with predictive ML — not with static LLM prompts. For more on how ChainAware’s predictive agents work in practice, see the Prediction MCP developer guide.

Try Real Utility AI — Free

ChainAware Fraud Detector — 98% Accuracy, Predicts Before It Happens

This is not LLM-based hype. ChainAware’s fraud detection is a proprietary predictive ML model trained on 14M+ wallet profiles across 8 blockchains. It predicts future fraudulent behavior — not past events. Free to check any wallet. No signup required.

Self-Custody vs Custodial: Why DeFi Solves a Real Problem

Before discussing AI agents in DeFi, Martin and Tarmo spend time on a foundational question: why does DeFi matter in the first place? The answer comes down to a single distinction — owning an asset versus owning a claim on an asset.

In traditional banking — and in centralized crypto exchanges — users do not own their assets. They own a record in a database that says the institution owes them those assets. The institution controls the actual assets. This is the custodial model. The bank or exchange holds your funds and gives you an IOU.

DeFi operates on self-custody. Users control their private keys directly. Consequently, they control access to their actual assets — not to a claim. Nobody can rehypothecate those assets, lend them out, or lose them without the user’s direct participation. As Martin explains: “In DeFi you have the asset instead of a claim on the asset. That is the difference between the custodial system — where you deal with claims on assets which belong to you — versus self-custodial, where you own the asset itself.”

This distinction matters enormously for risk assessment. Furthermore, it defines what makes DeFi valuable independent of any AI enhancement. Self-custody eliminates an entire category of counterparty risk that custodial finance inherently carries. For more on how ChainAware protects self-custodial DeFi users from the risks that do remain, see our complete KYT and AML guide for DeFi.

The MF Global Warning: Rehypothecation and Its Risks

Tarmo brings a specific historical case to illustrate the custodial risk. Before Credit Suisse, he worked at Man Investments — described as the largest independent hedge fund in the world at the time. Man Investments had a sister company called MF Global.

MF Global offered brokerage services to retail clients with approximately $600M in client deposits. Everything operated smoothly until the firm decided to speculate with those client assets — taking highly leveraged positions on interest rates. When those positions moved against them, clients logged into their accounts and found nothing. The assets were gone. MF Global had rehypothecated — lent out — the client funds to make its own trades. Rehypothecation in European jurisdictions allows banks to lend out client assets up to 80 times. The same asset can appear on 80 different books simultaneously.

Tarmo describes it vividly: “You have one cow and the bank can lend it out 80 times. The same cow is existing 80 times in the same moment in different books of different organizations.” When one link in that chain fails, nobody knows where the assets actually are. Celsius and other centralized crypto platforms repeated this exact pattern in 2022, with identical consequences for depositors.

DeFi eliminates this risk by design. On a DeFi protocol, the smart contract holds the assets — not a company. No human can decide to rehypothecate them. This is why, despite the volatility and fraud risks that DeFi faces, the fundamental architecture is a genuine improvement over custodial systems for users who want full control. For guidance on how to assess DeFi protocol security before depositing, see our rug pull detector guide.

What DeFi AI Actually Means

With the DeFi foundation established, the discussion turns to DeFi AI — and Tarmo’s definition is precise: “DeFi AI = digitalization by DeFi + superior decision making by AI agents. We add superior decision making to existing DeFi. DeFi already has utility. When we go over to DeFi AI, that utility is massively improved because of the superior decision power of AI agents.”

The evolution follows a clear sequence. First came digitalization — DeFi automated financial processes that previously required human intermediaries. Uniswap automated market-making. Compound automated lending and borrowing. Aave added flash loans. These products created genuine utility. However, decisions within these systems were still either fully deterministic (rules-based smart contracts) or made by human users who were often poorly informed.

On-Chain Data as an AI Advantage

DeFi AI adds a second layer: autonomous, learning agents that make better decisions than either static rules or average human judgment. Crucially, these agents train on freely available on-chain data. Tarmo highlights this advantage explicitly: “This data is free. It’s not like in traditional finance where you have to buy very expensive licenses to get data sources.” Every transaction on Ethereum, BNB, Solana, and other chains is publicly accessible, freely available, and continuously growing. An AI agent trained on this data can improve daily simply by relearning from new on-chain events — no data licensing fees, no API paywalls, no data moats protecting incumbents.

Additionally, the combination creates a win-win for all stakeholders. Users get better products that serve their needs more precisely. Protocols get better performance metrics — higher TVL, better conversion rates, lower fraud losses. Investors benefit from improved cash flows as the products outperform competitors that don’t use AI. As Tarmo notes: “When decentralized finance merges with AI agents, it is a win-win where everybody wins more out of it — which happens very seldom in the real world.”

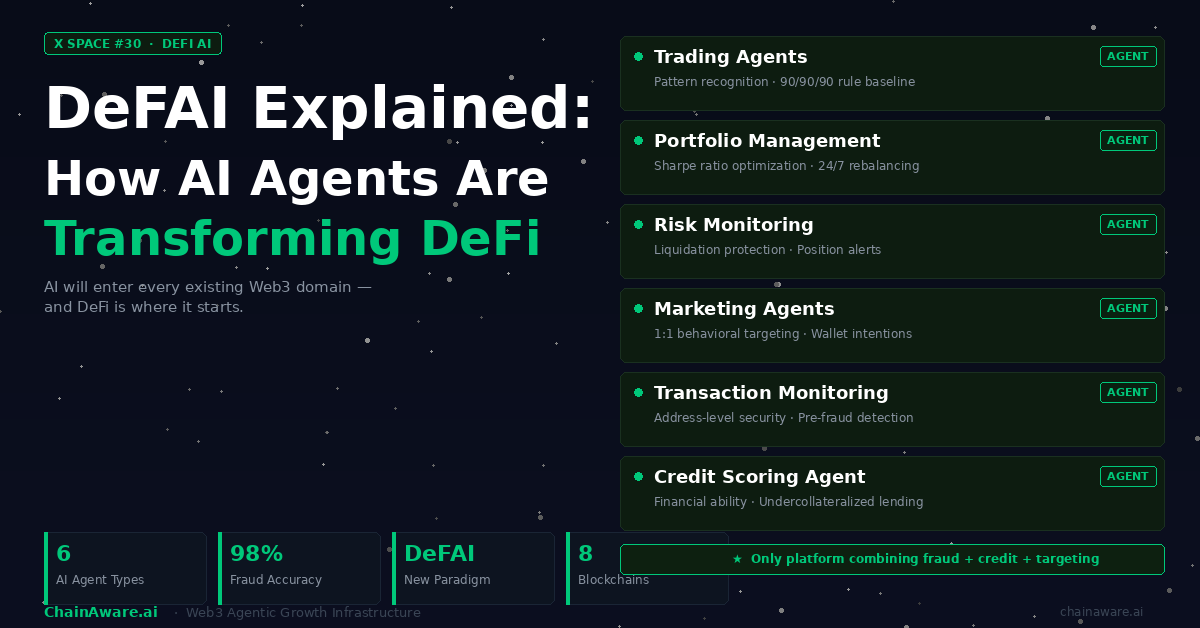

Six specific AI agent categories are emerging in DeFi. Each one takes an existing DeFi function and replaces human decision-making with AI-driven superiority. For how these agents integrate via API into existing platforms, see our guide to 12 blockchain capabilities any AI agent can use.

1. Trading Agents — Pattern Recognition at Scale

Trading agents are the most widely discussed AI use case in crypto. However, the discussion in X Space #30 cuts through the hype with a sobering baseline: the 90/90/90 rule. Ninety percent of traders lose 90% of their assets in 90 days. This is not speculation — it comes from Martin and Tarmo’s decade-plus experience at Credit Suisse and Man Investments, where professional trading infrastructure operated at a scale most retail participants never encounter.

Man Investments ran automated trading engines managing $20 billion in assets under management over 20 years ago. The systems that outperform human traders use predictive AI for pattern recognition — not LLMs. LLMs analyze language sequences. Trading requires pattern recognition across price data, volume data, liquidity data, and on-chain flow data. These are completely different data types requiring completely different model architectures.

Current trading systems in Web3 are largely rules-based — if/then/else conditions that attempt to encode human intuition as explicit logic. AI trading agents replace the explicit rules with learned patterns, potentially producing accuracy well above the 90/90/90 baseline. Moreover, unlike human traders, they operate 24/7 without fatigue, emotion, or variance. For more on the distinction between rules-based systems and genuine predictive AI, see our guide to real AI use cases for Web3 projects.

2. Portfolio Management Agents — Risk-Adjusted Returns

Portfolio management agents operate at a higher level than trading agents. Rather than managing individual positions, they manage the overall portfolio — balancing asset classes, monitoring correlations, and optimizing risk-adjusted returns according to the Sharpe ratio framework.

Martin and Tarmo bring their CFA (Chartered Financial Analyst) credentials to this discussion explicitly. The core insight from professional portfolio management is simple: generating returns is easy — anyone can take extreme leverage and win in a bull market. Generating risk-adjusted returns consistently is the actual challenge. The Sharpe ratio (return per unit of risk) is the correct metric, not raw return.

Currently, DeFi has no equivalent to the private banking wealth management layer. Users must manually monitor their positions across multiple protocols, rebalance when allocations drift, and manage liquidation risks independently. An AI portfolio management agent automates all of this — watching allocation ratios between asset classes, rebalancing when thresholds are crossed, and applying risk optimization logic continuously. Tarmo calls it “an automated wealth manager that works on your portfolio and rebalances it and keeps the risk minimized.” For context on how SmartCredit already deploys risk monitoring for its preferred clients, see the Credit Scoring Agent guide.

3. Risk Monitoring Agents — Protecting Individual Positions

Risk monitoring agents differ from portfolio management agents in scope. Portfolio management handles the full portfolio — risk monitoring handles individual positions, specifically the risk of liquidation in borrowing and leveraged lending protocols.

The liquidation problem in DeFi is real and costly. Protocols like Aave, Compound, and MakerDAO generate significant revenue from liquidating undercollateralized borrowers. Many of these liquidations happen not because borrowers are insolvent but because they lack tools to monitor their positions in real time and take protective action before the liquidation threshold is crossed.

A risk monitoring agent watches a user’s borrowing position continuously. When collateral value drops toward the liquidation threshold, it triggers alerts — via Telegram, webhook, or automated actions. Furthermore, it can be configured to take protective actions automatically: adding collateral, partially repaying the loan, or executing a hedge. This is the DeFi equivalent of a bank’s margin call team, but operating 24/7 with zero human latency. SmartCredit offers risk monitoring agents to preferred clients as part of their DeFi AI stack. For the technical implementation via MCP, see our guide to 5 ways Prediction MCP turbocharges DeFi platforms.

Protect Your DeFi Positions — 24/7 Monitoring

ChainAware Transaction Monitoring Agent — Real-Time Address Surveillance

Stop monitoring manually. ChainAware’s Transaction Monitoring Agent watches wallet addresses continuously — detecting pre-fraud behavioral patterns before they result in losses. Telegram notifications. ETH, BNB, Polygon live. Enterprise subscription.

4. Marketing Agents — Behavioral Targeting for DeFi

Marketing agents address the most expensive problem in Web3: user acquisition cost. Currently, acquiring one transacting DeFi user costs $1,000–$3,000 — a figure that makes most protocols structurally cash-flow negative. Traditional marketing approaches in Web3 — KOLs, airdrops, crypto ad networks — drive traffic but not conversion. Sessions from KOL campaigns typically last 12–15 seconds. Users arrive, see a generic interface, and leave.

ChainAware’s marketing agents solve this conversion problem through behavioral targeting at the wallet connection event. When a user connects their wallet to a DeFi platform, the marketing agent immediately calculates that wallet’s behavioral profile from on-chain data: what protocols have they used, what is their experience level, what are their predicted next actions? Based on this profile, the agent generates a personalized message — an embedded section of the website that resonates specifically with that user’s intentions.

Resonance, Not Interruption

Martin describes the goal: “You have to resonate with users, not users resonate with you.” A yield-farming-experienced wallet visiting a lending platform should not see a generic “earn up to 15% APY” banner. Instead, it should see messaging tailored to its specific experience and likely next action. This one-to-one targeting — at scale, automated, without cookies or identity — is the Web3 equivalent of what Google AdWords did for Web2.

Additionally, the power law distribution in DeFi — where a small number of protocols capture the vast majority of TVL and users — starts to flatten when effective targeting reaches smaller protocols. Users currently gravitate to large protocols partly because visibility drives familiarity. When a smaller protocol with genuinely better terms can reach exactly the right user with exactly the right message, the competitive dynamic shifts. For a detailed guide on how marketing agents work, see our Web3 behavioral user analytics guide and our analysis of why personalization is the next big thing for AI agents.

5. Transaction Monitoring Agents — Address-Level Security

Transaction monitoring agents provide security at the address level — and the Bybit hack, referenced explicitly in the X Space, illustrates why this matters more than contract-level security.

After major DeFi hacks, discussion typically focuses on smart contract vulnerabilities. Auditing firms audit the code. Protocols get 15 different audits from different firms. Yet hacks continue. Tarmo explains why contract monitoring alone is insufficient: “What you need is monitoring of addresses. Fraudulent addresses are doing nasty things. Avoid transacting with these partners who use those addresses. It is your firewall.”

Behind every malicious contract sits a malicious address. Moreover, regulators increasingly mandate address-level monitoring specifically — not contract monitoring. FATF’s guidance on virtual assets focuses on user addresses as the unit of compliance obligation, not smart contract code. Monitoring addresses catches bad actors before they can deploy or interact with malicious contracts.

ChainAware’s transaction monitoring agent does this continuously. It monitors wallets connecting to or transacting with a DeFi platform, detects when behavioral patterns shift toward pre-fraud signatures, and sends real-time alerts. Critically, this is predictive — it identifies the behavioral change before any fraud occurs, not after. ChainAware integrates via Google Tag Manager pixel, requiring no code changes to existing DeFi front-ends. For the full integration guide, see our AML and transaction monitoring integration guide for DApps.

6. Credit Scoring Agents — Financial Ability Assessment

Credit scoring agents perform a function that traditional finance has relied on for decades — assessing the financial ability of a borrower — but applied to anonymous on-chain wallets without any KYC.

Martin clarifies what credit scoring actually measures: “It’s not just — is someone now paying back what they borrowed? It’s a general financial ability of a person. What is his financial ability?” A FICO score in traditional finance captures income, debt levels, payment history, and account longevity — a composite measure of financial health, not just loan repayment history. ChainAware’s credit scoring agent does the same from on-chain data.

For DeFi lending protocols specifically, credit scoring unlocks a critical capability: undercollateralized lending. Today, nearly all DeFi lending is overcollateralized — borrowers post 150% collateral to receive a 100% loan. This constraint exists precisely because there is no credit infrastructure to assess borrower quality. By integrating credit scoring agents, lending protocols can offer better terms to high-creditworthiness wallets and tighter terms to lower-quality ones — personalizing risk management the same way traditional banks do for customers with different credit scores. Furthermore, credit scoring extends beyond lending to ABC client filtering, growth targeting, and collateral decisions across any DeFi protocol. For the complete guide, see our complete Web3 credit scoring guide.

SmartCredit: A Live Example of DeFi AI

Throughout X Space #30, SmartCredit.io serves as the concrete live example of what a fully integrated DeFi AI platform looks like. Martin and Tarmo built SmartCredit before ChainAware — and it incorporates AI agents across every function the X Space discusses.

SmartCredit was the first DeFi lending protocol to offer fixed-interest, fixed-term loans — an innovation that Traditional DeFi, with its variable-rate money markets, had never addressed. Fixed terms allow borrowers to plan: “I know exactly what interest I will pay.” Variable rates in DeFi lending are equivalent to a variable-rate mortgage where you never know what next month’s payment will be.

Beyond this core innovation, SmartCredit integrates the full DeFi AI stack. It uses transaction monitoring agents for security. It deploys credit scoring agents for borrower assessment. It leverages Web3 marketing agents for user conversion. Risk monitoring agents protect preferred clients’ individual positions. As Martin summarizes: “It is like an example of what future DeFi systems will look like. Integrate marketing agents, integrate transaction monitoring agents, integrate credit scoring agent, risk monitoring agent — and then you get superior performance compared to platforms which don’t use AI capabilities.” To understand how SmartCredit has applied these tools with measurable results, see the SmartCredit case study.

Access All 6 DeFi AI Agents via MCP

ChainAware Prediction MCP — Trading, Portfolio, Risk, Marketing, TM, Credit

ChainAware’s Prediction MCP server exposes all 6 DeFi AI agent capabilities as callable tools. Any MCP-compatible AI agent — Claude, GPT, custom LLMs — can call fraud detection, behavioral targeting, credit scoring, rug pull detection, and AML in real time. 31 MIT-licensed agent definitions on GitHub.

The Washing Machine Analogy: AI Frees Humans for Innovation

One of the most memorable moments in X Space #30 is Tarmo’s washing machine analogy for AI’s broader societal impact. He asks: “Which technology enabled cave-to-humans most freedom of time?” His answer: the washing machine. Before it existed, manual laundry consumed enormous amounts of daily time. The washing machine automated that task completely — and the time freed up went toward innovation, not unemployment.

AI agents do the same at the expert level. Tasks that currently require skilled employees — compliance review, fraud analysis, portfolio rebalancing, user targeting — will be taken over by AI agents operating with superhuman accuracy. The freed time then goes toward what humans do best: creative work, new product development, new startup formation, new ideas. Martin adds: “People will have more capacity to do what they are best at. This is creation of new concepts, new startups, new ideas, new products.”

Consequently, the fear that AI creates unemployment is misplaced — at least for builders and founders. The analogy holds precisely because the washing machine did not reduce human activity; it redirected it toward higher-value creation. AI agents in DeFi will similarly redirect human effort from repetitive expert-level tasks toward genuinely creative ones. For more on this transition in the context of AI agent infrastructure, see our article on the Web3 agentic economy.

Comparison: Attention AI vs Real Utility AI in DeFi

| Dimension | Attention AI (Fake AI) | Real Utility AI (DeFi AI) |

|---|---|---|

| Core technology | LLM prompts, 2–3 lines of code | Proprietary predictive ML models |

| Accuracy | Unmeasurable — outputs may hallucinate | Measurable, backtested (e.g. 98% fraud accuracy) |

| Competitive moat | None — easily copied in hours | Strong — years of training data and model iteration |

| Problem solved | Narrative for token speculation | Specific measurable DeFi problem (fraud, acquisition, liquidation) |

| Continuous improvement | No — static LLM prompts | Yes — daily retraining on new on-chain data |

| Domain | Creates new attention-based categories | Enters and enhances existing DeFi domains |

| Revenue model | Token speculation | Enterprise subscription, API access |

| Market cycle resilience | Collapses in corrections | Survives — utility drives ongoing demand |

| ChainAware example | — | Fraud detection, marketing agents, TM, credit scoring |

| Data source | Generic training data | Free, public on-chain data — continuously updated |

| User benefit | Speculative token upside only | Lower acquisition cost, higher security, better rates |

Frequently Asked Questions

What is DeFi AI and how is it different from regular DeFi?

DeFi AI combines the automated financial processes of decentralized finance with AI agents that make superior decisions within those processes. Regular DeFi uses deterministic smart contracts — rules that execute the same way every time. DeFi AI adds learning agents that analyze on-chain data, predict user behavior, detect fraud, optimize portfolios, and improve marketing — continuously getting better as they process more data. The result is higher utility for users and better economics for protocols. For a full breakdown, see our guide on real AI use cases for every Web3 project.

What is the difference between attention AI and real utility AI?

Attention AI combines buzzwords — “decentralized AI cross-chain optimization” — to attract investor interest without delivering real utility. Real utility AI uses proprietary ML models to solve specific, verifiable problems with measurable accuracy. The test is simple: can you state what problem the AI solves, measure its accuracy, and verify that the product is live with real users? If yes, it is utility AI. If the answer to any of those questions is no, it is attention AI.

Why are LLMs insufficient for DeFi AI decision making?

LLMs are statistical autoregression models optimized for language patterns — predicting which word comes next in a sequence. They are excellent for generating text, summarizing documents, and answering questions. However, they are not designed for on-chain behavioral prediction, fraud detection, or trading signal generation. Those tasks require predictive ML models trained on specific data types (transaction patterns, behavioral signals, price data) with backtested accuracy scores. Using an LLM for fraud detection is analogous to using a spell-checker to predict stock movements — technically possible to attempt, but structurally wrong for the task.

What is rehypothecation and why does it matter for DeFi?

Rehypothecation is the practice of lending out client assets to generate additional returns. In European banking, a single asset can be lent out up to 80 times simultaneously. MF Global used client deposits (approximately $600M) for speculative trades — when those trades failed, clients lost everything. Celsius repeated this pattern in crypto in 2022. DeFi eliminates this risk structurally: self-custodial protocols cannot rehypothecate user assets because no central entity controls them. Users hold their private keys and retain direct access to their assets at all times.

How does ChainAware’s marketing agent reduce DeFi user acquisition cost?

ChainAware’s marketing agent calculates each connecting wallet’s behavioral profile from on-chain data — experience level, protocol history, predicted intentions — and generates personalized messages that resonate with that specific user. Instead of every visitor seeing the same generic banner, each user sees a message tailored to what they are likely to want to do next. This resonance drives higher engagement, longer session duration, and better conversion rates. The result is a significant reduction in cost-per-transacting-user compared to mass broadcast approaches like KOLs and crypto ad networks. For measured results, see the SmartCredit case study.

What makes ChainAware’s AI cross-category in Web3?

Every Web3 project — regardless of category — needs two things: users and security. Marketing agents reduce user acquisition cost in every category. Transaction monitoring agents improve security in every category. These are not DeFi-specific problems; they are universal Web3 problems. Consequently, ChainAware’s infrastructure applies to gaming, NFTs, payments, gambling, wallets, and every other Web3 domain — not just DeFi. This cross-category applicability is what Martin calls “the real AI revolution”: the same agent infrastructure benefiting every existing Web3 domain simultaneously. For more on ChainAware’s full agent ecosystem, see the MCP integration guide.

Is the free ChainAware analytics useful for DeFi projects?

Yes — the free Web3 User Analytics dashboard is the starting point for any DeFi project wanting to understand its actual user base. It shows the behavioral profile of connecting wallets across eight dimensions: intentions, experience levels, risk profiles, protocol history, fraud distribution, and more. Many DeFi teams discover that their assumed user base (e.g. experienced DeFi participants) and their actual user base (e.g. low-risk retail traders) are completely different — which fundamentally changes marketing and product strategy. The free analytics tier is available to any DeFi project via Google Tag Manager integration. See the complete analytics guide to get started.

Start Building DeFi AI — Free Analytics + Enterprise Stack

ChainAware.ai — Web3 Agentic Growth Infrastructure

Free User Analytics → Marketing Agents → Transaction Monitoring → Credit Scoring → Rug Pull Detection. All 6 DeFi AI agent capabilities in one platform. Start free in 2 minutes via Google Tag Manager. 14M+ wallets. 8 blockchains. 98% fraud accuracy. 31 open-source agents on GitHub.

This article is based on X Space #30 hosted by ChainAware.ai co-founders Martin and Tarmo. Watch the full recording on YouTube ↗. For questions or integration support, visit chainaware.ai.